Receiving a Notice of Federal Tax Lien can be intimidating. Luckily, a professional tax attorney can help you navigate your taxes and help you determine your options.

As an agency of the United States government, the IRS has unique tools at its disposal to collect tax payments – especially in cases of particularly tardy or late dues, or significant tax debt. In some cases, they will follow up payment demands with a Notice of Federal Tax Lien.

While intentionally avoiding the IRS and one’s taxpaying duties can be a civil and criminal offense, the IRS also recognizes that most cases of taxpayer debt don’t occur due to malice or illegal intent, but instead may be the result of dire extant circumstances. Other cases of tax debt may be due to one or two years of hardship causing a temporary pause in payments.

What is a Notice of Federal Tax Lien?

The government needs to collect what it’s owed – and slowly close the tax gap. To this extent, the IRS files federal tax liens every year to taxpayers owing more than $10,000 in taxes, up from its $5,000 debt threshold prior to the Fresh Start Program initiated in 2011.

These liens do not directly force action on part of the taxpayer or any other organization, but are certainly a cause for alarm, as they represent the government’s claim on all of a taxpayer’s assets and properties until their debt is paid. To file such a lien, the government issues a public document called the Notice of Federal Tax Lien.

Defining a Federal Tax Lien

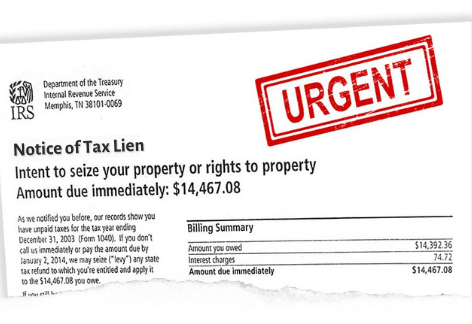

When the government issues a Notice of Federal Tax Lien, it files a public document with the local recording office that specifically identifies the taxpayer’s tax liabilities and declares the lien itself.

This document isn’t sent to the taxpayer – instead, it’s legal document that becomes a matter of the public record, and establishes that the US government’s rights to the taxpayer’s assets and property supersede the claims of any and all other creditors, unless established otherwise, and until the tax debt is paid (or certain other requirements are fulfilled).

At the same time, the taxpayer is sent a Notice of Federal Tax Lien Filing, and Your Right to a Collection Due Process Hearing. As it is within your rights as a taxpayer, you may appeal against a lien if you find that the IRS filed one incorrectly. In most cases, your best bet of having a lien removed is to begin paying your tax debt. Depending on your circumstances, the IRS may remove a federal tax lien before your debt is fully paid, provided you have been making payments on time and are up-to-date with all your current and incoming tax returns and dues.

In other words, until you pay your debt or make an effort to pay your debt, the equity of nearly everything to your name is claimed by the US government. Until such a lien becomes a levy, the government does not swoop in to take what you own.

Instead, a federal tax lien ensures that should you sell your home or go bankrupt, the IRS will be first in line to satisfy your tax liability with the value of what you’ve liquidated, before anyone else can claim their share, including you.

Liens vs. Levies

Liens can become levies, and the government will typically try to coerce payment through a lien before it resorts to a levy. Where a lien is a legal claim on the value of what you own, a levy is the legal seizure of an account, property, or portion of your income.

Levies are one of the last tools the IRS will use to claim tax liabilities, as levies involve physically claiming and selling property, emptying bank accounts, or making employers withhold a portion of a taxpayer’s wages.

If the total value of a home or account exceeds that of your debt, the IRS will pay back the difference. Otherwise, if it isn’t enough, they may issue another levy. Like liens, levies can be halted, provided you take appropriate action within the timeframe given by the IRS.

Tax Liens and Credit Reports

Starting in 2017, the three national credit bureaus (Experian, Equifax, and TransUnion) eliminated tax liens from consumer credit reports and announced that federal tax liens would no longer automatically show up on your credit report.

Prior to this change, a tax lien (given that it is public information) would be added to your credit report, not only affecting your ability to file for a loan or apply for credit while under the effect of the lien (as the US government would supersede any creditor), but continuing to affect your consumer credit score for up to about seven years after the lien was lifted.

This gave additional weight to liens, as they would leave a considerable and lasting impact on your ability to seek financing and refinancing following the government’s claim.

However, this practice halted after internal studies apparently led the credit bureaus to find that many credit reports were wrongly affected by tax liens due to clerical errors.

Just because a lien doesn’t show up on your credit report anymore doesn’t mean that it won’t have a lasting negative financial impact. As mentioned, lenders and credit companies will still ask about any existing tax lien against your assets and property, which can affect your options and any potential interest rates you might have to face when applying for a loan.

Seeking Assistance for a Federal Tax Lien

If you have received a Notice of Federal Tax Lien, your first move should be to contact a financial and tax professional. You have multiple options for tax lien removal, even if you don’t have the means to pay off your debt at the moment.

Other options include arguing for a Currently Not Collectible status, making an Offer in Compromise, getting a lien discharged on specific property to seek financing, subordinating a lien in favor of another creditor to secure a loan, and more.

At Rush Tax Resolution, our tax professionals can help you navigate these options and the IRS’s ruleset, and help ensure that you resolve your tax debt situation as smoothly as possible.